Schlumberger: Big Blue Revving The Engines In 2022

Years of under-investment in upstream energy could create initiate a strong expansion cycle for oil and gas, benefitting this energy service giant.

It would be hard to find a quarterly report with more reasons for optimism than the one Schlumberger, (NYSE:SLB) delivered for Q-3. It was the confirmation of my thesis, that although the market has yet to reward the service players with the multiples it has bestowed on the producers, that time may not be far off. Their stock immediately declined from about $35 to the high $20’s. Covid concerns and some wishy-washy commentary from OPEC, along with about 2-months of inventory builds helped to put a damper on energy stocks. It’s been a painful slog for holders of SLB stock the last couple of years, but I think brighter skies could be on the horizon.

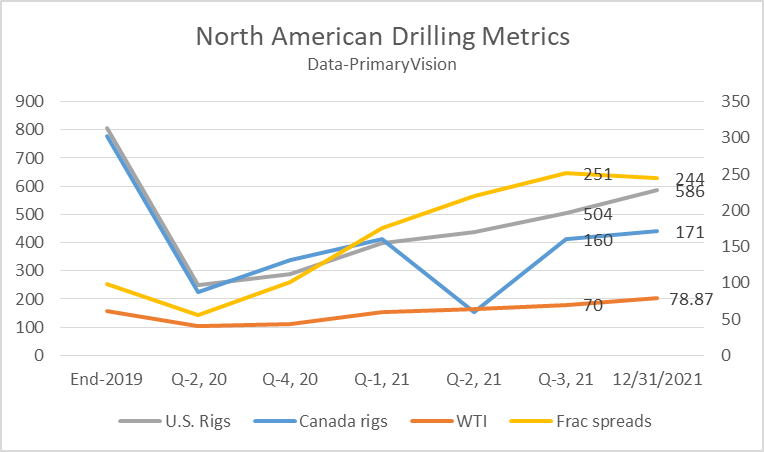

After essentially treading water for Q-4, in spite of improving fundamentals-WTI/Brent/Rig count/Frac spreads, etc, the stock has moved back toward the upper end of its recent range.

Chart by author

Note the line for rigs vs frac spreads will cross soon, indicating a pivot toward drilling. For the past couple of years, shale output has been largely maintained through Drilled but Uncompleted wells (DUC’s) withdrawal-down 50% over the past year. This is reaching a balance point, and I expect the rig count to push through the 600 level early this year.

In this article we will review the Q-3 numbers and the commentary by SLB management, and develop an opinion about the propects for continued growth in the company. We will also see if we can see a catalyst that will improve the chance of capital growth in the stock. Big Blue will release Q-4 earning on Jan, 21. A pleasant surprise could be in store.

The thesis for SLB

Big Blue is the largest of the oilfield service companies-OFS, with twice the capitalization of its nearest competitor, Halliburton, (NYSE:HAL). The central thesis for buying the stock now-it's tripled since the lows of 2020, is continued growth in its markets domestically and internationally. Both baskets of oil-WTI and Brent have made solid moves out of the $50's-where the payouts are just adequate on most projects, to the middle and upper $80's-where payouts are simply stunning on an expanded list of projects, and operators are reporting tens of billions in run rate free cash flow. If you haven’t read it, you should read my report on Pioneer Natural Resources, (NYSE:PXD), to get a flavor of the massive cash flow being generated at current WTI prices. (Just click the link).

The magnitude of this change has not fully settled on the investment community as yet...but it's beginning to as this WSJ article notes-

A surge in energy stocks is challenging climate-conscious money managers who beat the market for years when the sector struggled but are now missing out on Wall Street’s hottest trade.

A final point here is the bullishness of management about the year to come. The days where CEO’s pump their stock regardless of actual market conditions are gone. These folks have to follow strict disclosure rules that have teeth-fines and jail time hanging in the balance for those who stray over the line. This not to say they don't bury stuff in a 10-Q, they do. But when it comes to forward looking commentary, I find they are fairly circumspect. Particularly SLB's new CEO, Olivier Le Peuch. He has all the hucksterism of a mortician. Here's Ollie on 2022-

Now I would like to close my prepared remarks with our earliest view of 2022. Against the backdrop of the constructive environment I described earlier, our confidence in the onset of an exceptional growth cycle is reinforced. At this early point in the planning cycle, and absent of setbacks in economic and political recoveries, we anticipate very strong global upstream capital spending growth.

That is decidedly bullish commentary and comes from the guy who told you this in 2020.

Despite the recent agreements by the world’s largest oil producers... Q2 is likely to be the most uncertain and disruptive quarter that the industry has ever seen," Le Peuch said during today's earnings conference call.

So let's give Ollie credit for telling it like it is. If he says we are going to "rip and run," well then by golly, you'd better get your track shoes on!

SLB Q-3

Revenue rose 4% to $5.8 bn, but missed analyst expectations by $90 mm. Cash flow from operations rose to $1.107 bn and free cash came in at $671 mm, each down from Q-2 thanks to a large tax refund of $437 mm received then. EBITDA margins rose to 22.2%, up 90 basis points from the prior quarter. Debt fell to $14.3 bn in the quarter, down by $1.3 bn from Q-2, and over $1.5 bn since the beginning of the year. The company has $2.942 bn of cash on the books.

Among the company's 4-divisions, 2 out of 4 saw improvement over the prior quarter.

Digital Integration was flat at $812 mm.

Reservoir Performance rose 7% to $1.2 bn.

Well Construction was up 8% to $2.3 bn and lead by improvement in North America and international land and offshore.

Production systems was flat at $1.7 bn.

North America accounted for $1.13 bn, led by strong increases in drilling and completion activity. International revenue of $4.68 billion grew 4% sequentially and 11% year-on-year. The sequential revenue increase was led by double-digit growth in Latin America complemented by sustained activity in the Europe/CIS/Africa and Middle East & Asia areas. In North America, revenue of $1.13 billion grew 4% sequentially and 9% year-on-year. The sequential growth was driven mainly by a strong seasonal rebound in land drilling, higher Asset Performance Solutions (APS) revenue in Canada.

Capex for 2021 is expected to land out at $1.6 bn. A dividend of $.125 per share was approved in line with previous.

SLB filings

Some key contract wins

SLB has received a multi-year, multi-billion dollar contract from KSA to provide stimulation and ancillary services in their Al-Jafurah super-giant (300 TCF) gas field development. Mobilization is expected to start in the fourth quarter of 2021.

In Oman, The Petroleum Development Company of Oman, has awarded SLB a 5-year contract with up to 2, 2-year extensions for as many as 350 wells in a high pressure gas field. This work is expected to commence in Q-4, 2021.

Kuwait Oil Company awarded SLB a five-year supply agreement for wellheads, production trees, and services for 230 new wells and 250 workover wells in the country's deep Jurassic formations. The scope of the agreement includes the supply and installation services of 15,000-psi high-pressure, high-temperature (HPHT) wellheads, production trees, chokes, and control panels.

Turkish Petroleum has given SLB a contract for Phase-1 development of the offshore Sakarya field. The integrated project scope will cover subsurface solutions to onshore production, including well completions, subsea production systems (SPS), and an early production facility capable of handling up to 350 MMscf/d of gas. This is the country's largest gas field.

In Brazil, Petrobras awarded Schlumberger a contract for integrated completions on 21 wells in presalt concessions. Presalt well are deep, and hot and require advanced technology to drill and complete. The intelligent completion design chosen for these wells includes a selective open hole lower completion, integrating a premium isolation valve and downhole interval flow control valves and a Metris* permanent monitoring system. The Formation Isolation Valve shown in the pic below can be functioned from a Floating Production Storage and Offloading-FPSO vessel, to open and close. This enables flowing of the well and positive shut off when complete. This is an absolutely critical to installing subsea completions.

Premium ISO Valve (Watch the vid.)

Intelligent completions are done to enable rigless sleeve and valve shifting, and will enable Petrobras to enhance ultimate recovery in these higher-pressure reservoirs by more accurately monitoring and controlling production. Installation is expected to commence in the third quarter of 2022.

These are illustrative of the type of work the company is getting now, and ties in with the bullishness of Le Peuch's statement above. Compare that with the 1-off satellite wells the company was getting a couple of years ago. The revenue potential is night and day.

Risks

Obviously Schlumberger carries more market risk at ~$35 than $12, its lows of Q-2, 2020, level. That said, I think the downside is limited in the current oil price scenario. The key risk is that it could dither in the mid-$30's, tieing up capital as doubts about the future of oil and gas percolate in investors minds.

The analyst community remains bullish with a median target of $35, slightly below where it is now, and a high of $48. Obviously a push toward the higher number is a reason to stay long the stock at present levels.

I see a couple of possibilities here. One, the rise in oil and gas prices is dramatic over the past year. WTI and Brent have doubled thanks to government disincentivizing new drilling, reduced capex for exploration, falling inventories, and a stronger than expected Covid recovery. There is an almost certainty of a significant pull back at some point as we are approaching historical demand destruction levels in commodity prices. Significant increases in drilling, capital budget reflation, alternative fuels will put in a top. They always have. In that scenario wherever it is SLB stock will top out...if it plays out. Is it different this time? Maybe.

Two, inflation is finally here, after a 20-year era of disinflation. Stocks don't do well historically as cost inputs go higher. Government issued securities begin to provide a lower risk alternative to stocks. Higher costs compress margins and reduce multiples investors are willing to pay for ownership of companies. Not all sectors suffer proportionately though. Some out-perform while others lag behind. Who benefits in a higher interest rate environment? Often financials and companies participating in the upswell of commodity prices-energy companies in particular.

These are risks, not certainties and a possible catalyst could come into play, that will push the demand destruction goal post way deep into the end zone. There's now talk of $110 WTI and $120 Brent as being the new level of demand destruction.

The catalyst that could push oil and gas prices higher for longer

I've documented in the past that years of under-investment in legacy energy sources-new supplies of oil and gas are about to come home to see the global energy mix…in a bad way. I came pretty close to the mark in my predictions here.

I won't beat the drum any louder here. I am sure you get the point that's been brought so roundly into focus this fall as green energy sources showed their weakness. Particularly in Europe and the Uk. As intermittent supplies, they are subject to the whims of the environment. When the wind doesn't blow... What's been brought sharply into focus in people's minds is the need for dependable back up to alternative energy. That means oil and gas, and thanks to the supply/demand deficit that's going to mean drilling. And, that will put money into SLB's pockets.

A final point for enthusiasm about oil prices in 2022. Crude stocks as per the most recent release of the EIA-Weekly Storage and Production Report, (WPSR), shows clearly that as we enter 2022, stocks are significantly below 5-year averages.

Your takeaway

There is no question that SLB is selling for a high multiple- EV/EBITDA is ~11.3. As debt declines and OCF increases though the case for a growth driven, higher multiple is in play. That high end target of $48 is pretty tempting to me, and would only require a multiple of 14-15 to obtain. That seem doable in this environment. I am going to stick it out and stay long.

Disclosure. The author is long SLB.

Disclaimer. Nothing I say in this article should be construed as investment advice. It may look or sound like it, but it is not. I am not a CPA/CFA and have no formal training/certifications/licences in either discipline. In these articles I present analysis and relevant information that an interested investors may find instructive. I may be bullish, bearish, or neutral and will discuss why, but I am definitely not recommending you buy or sell any security I discuss. Investors should always do their own due diligence before plunking down their hard-earned cash. They alone are responsible for their investing decisions.