Pioneer Natural Resources: Printing Cash In The Permian

Great rock, scale, and logistics make for a compelling investment thesis

The hot take on Pioneer Natural Resources, (PXD)

Pioneer Natural Resources, (PXD) is one of the premier shale fracking companies in the U.S. It is in an elite group of 6-8 companies that have been making smart acquisitions the last year or so, that "bolt-on" to existing acreage positions with Tier I locations ready to drill. These companies are getting ready to report massive cash flow increases, on top of relatively flat capex, that are going to rock the analysts' socks. Multiples and share prices will launch higher as a result. PXD is at the top of the heap.

With an outstanding inventory of Tier I acreage with some 15,000 identified Tier I drilling locations, much of which in the Midland basin is privately held. This frees it from worries about fracking limitations that exist on federal lands. This high quality acreage combined with superior logistics-PXD has dedicated frac fleets through ProPetro (PUMP), local sand mine, and its own water distribution pipeline and recycling services, and leading edge drilling and completion practices, creates a low cost of production and high capital efficiency. All of this gives PXD a breakeven cost in its core Midland area of $28 per barrel. This enabled the company to post nearly $700 mm of free cash flow for 2020, on price realizations below $40 per barrel.

With price realizations nearly 80% higher for Q-4, 2021, PXD is printing cash and has a policy to return much of it to shareholders.

What drives the growth thesis for PXD?

PXD has rallied nearly 100% since the beginning of the year. Shares hit the mid-$190’s in October, but have pulled back since. I have previously identified a number of attributes that will drive success in shale drilling.

Great rock. Nothing can change what nature provides or leaves out. Tier I locations require less capital to develop and deliver increasing capital efficiency.

Scale. Having a massive, blocky acreage footprint is a key driver of success that enables longer laterals, and cuts cost. The lower costs of production will determine winners from losers.

Logistics. Being able to optimize the delivery of key elements of fracking-sand, water, pumping drives down costs over time.

Technology. Understanding the resource and how best to develop it through improved well spacing, longer laterals, and sand placement are critical features of success.

Access to markets. This speaks for itself. A successful company must be able to export its production to remote markets on the Texas Gulf Coast.

PXD ticks all of these boxes and through recent acquisitions-WPX Energy, and DoublePoint Energy, has built up a massive acreage base in the Midland basin.

The divestitures mentioned above have both closed as of this writing. This could spell an outstanding payday for investors in Q-1, 2022. We will discuss in the section on dividends.

Analysts are high on the company with 26 of 32 covering the company rating it a buy. Price targets range from a low of $197 to $305. I will put my own price projection in the closing section of this report.

Smart management a key driver

One of the things that nearly brought down the shale industry over the last few years of low prices, was growth at any cost fueled by bank debt. That model has been discarded in favor of capital restraint that maintains, or slightly increases production to match demand. It relies on cash flow to fund capex. As a shareholder, I like this approach as does the analyst community.

Only modest growth is baked into this forecast, and management has been pretty explicit on the subject of trying to chase the oil price with capital. This was raised in the Q-3 analyst call, and CEO Scott Sheffield, smacked it down-

No. I did mention of always - I did not mention anything about growing above 5%, so I've stated publicly that we're not going to grow above 5%. In regard to the macro, I do think that we're getting in a very tighter market over the next several years. Unused capacity in OPEC Plus is going to be used up in the next two years, there is no extra supply.

PXD filing

So let's pull the plug on any rumors that PXD will pick up 20 rigs in the new year to grow production appreciably beyond 5%. I think this fits well into the price/supply thesis for 2022 I advanced in my opening report.

Dividends and share buybacks

This is an area where PXD stands above the crowd. After a small chunk of free cash for growth capex and balance sheet repair, the overwhelming bulk of free cash goes to investors in the form of base and special dividends.

I’ll let CEO Scott Sheffield speak here on the subjects of dividends and share buybacks, with quotes taken from the Q-3 conference call-

We're starting to see additional dividend funds invest. We're starting to see our ownership change more and more dividend funds are buying PXD stock for the dividends. Secondly, we're starting to see more retail come in. We're making all that effort to go into all the firms trying to get more retail to shift into PXD because of the dividend yield.

“Retail,” that’s you and I. The “little guys” of the investing world are turning to companies like PXD for yield. This is historically a risky practice that leaves portfolios in tatters and investor’s in tears as 401K and IRA balances crash. What is noteworthy, and perhaps makes it different this time is that PXD is funding the base dividend on a much lower crude prices than we are expecting. The variable is funded on free cash flow and will rise and fall according to that metric.

We do think it's important over the next five years, if we do generate $25 to $35 billion of free cash flow, that we significantly reduce the share count over time. But it's going to be opportunistic and during market dislocations.

I think going forward, we stated our new debt targets that used to run debt - to-EBITDA 0.75, we lowered it to 0.5 and I'd prefer to have zero debt long term. It gives us a lot of options. I've stated already on the buybacks, we'll like to reduce shares significantly, but I'd like to do it at a good price. We think definitely we will be buying back cheap. And we've had several dislocations during 2021. It wouldn't surprise me if we have some dislocations during 2022. So you'll see us be buying shares in the marketplace during 2022.

I have a love and hate relationship with share buybacks. I love the idea of a reduction in share count. But, I hate the idea of buying high, which what often happens when cash is available for this sort of thing. Scott Sheffield agrees with me on this score as noted above.

The balance sheet

PXD is not overly laden with debt, with ~$6.0 bn of long term debt on the books. With the maturity schedule shown below, PXD is in a good position to retire debt with cash as it comes due. PXD has paid down over $500 mm in 2021 and expects to continue quarter by quarter and exit 2022 debt free. Scott Sheffield comments regarding plans for the balance sheet-

Preserving a strong Balance Sheet, as I mentioned earlier, we'll have the best Balance Sheet in the Company's history by the end of this quarter. And secondly, we move into zero debt by the end of 2022.

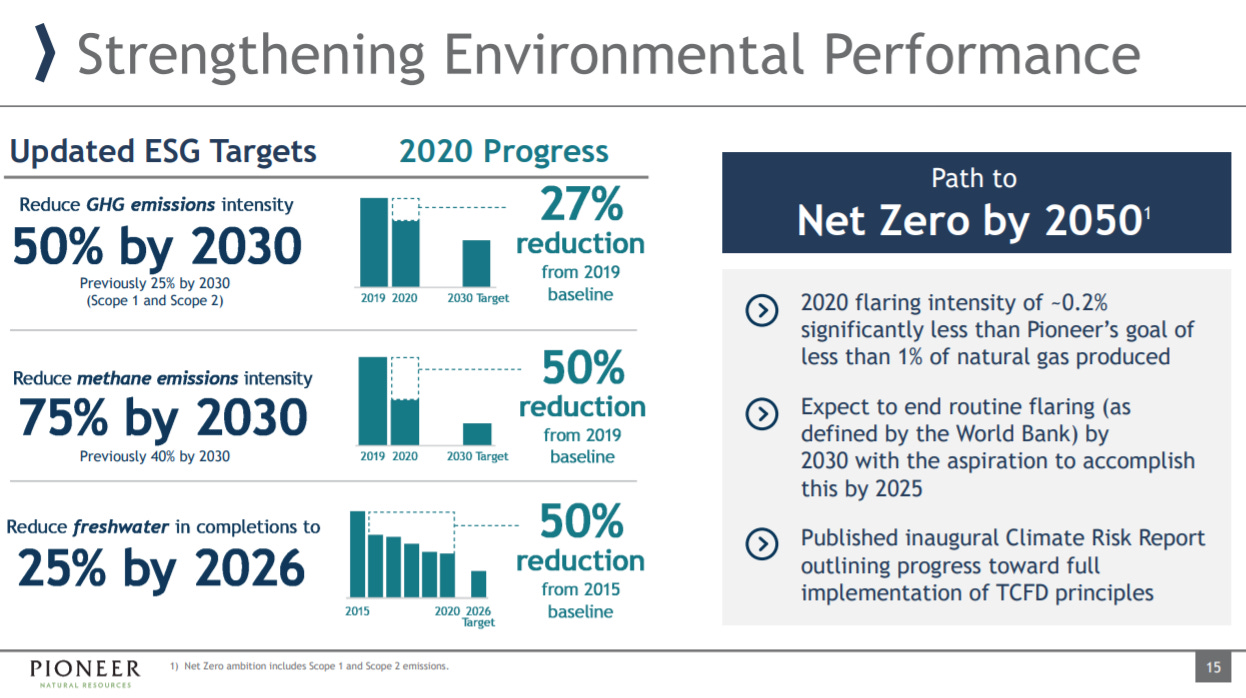

ESG

All oil companies have a responsibility to reduce their carbon footprint. PXD is taking steps in this regard, but is not engaging in transformative behavior as are some European oil companies. In my view this is the right approach and investors seem to agree.

Your takeaway

PXD is trading higher today on top of a massive, ~$6.00 per share rise on Monday. Yesterday we gave a little of that back, but seem be moving higher as trading opens today.

You can tell I am impressed with the approach the company has taken as regards shareholder, and development of their asset base. Management matters in this business. Knowing your mission matters as well, and I give PXD high marks in each case.

As I indicated early the company is going to see a massive cash flow increase thanks to the divestitures noted above. Quick back of the envelope calculations suggest free cash in the neighborhood of $6-7 bn for Q-4. The special dividend for Q-3 was $3.02 per share. If we see 80% of free cash flow applied to that $6-7 bn figure, investors could be in for a payout more than double that of Q-3. An announcement will be coming on this in late January, I expect the stock will break through the $200 level by then, if it hasn’t before.

Alright here's the part you've been waiting for. How do we put a valuation on the stock? The company had about $500 mm of hedging losses to pay for up for in Q3, but are essentially unhedged for 2022 , and intend to remain that way. These losses should diminish for Q-4, but will be dwarfed by free cash, as they were for Q-3.

Today PXD is trading at ~6.5X OCF. To get to the $305 share price that multiple will need to go to 9.15. With growth planned at up to 5% depending I'm sure on oil prices, it doesn't seem like a huge stretch.

I maintain that investors looking for growth and solid, above average income over the next few years, should put PXD on their alert list for dips. We're in one now, and I don't expect it to last for long.

Disclosure. The author is long PXD.

Disclaimer. Nothing I say in this article should be construed as investment advice. It may look or sound like it, but it is not. I am not a CPA/CFA and have no formal training/certifications/licences in either discipline. In these articles I present analysis and relevant information that an interested investors may find instructive. I may be bullish, bearish, or neutral and will discuss why, but I am definitely not recommending you buy or sell any security I discuss. Investors should always do their own due diligence before plunking down their hard-earned cash. They alone are responsible for their investing decisions.