Talos Energy: Ready To Rip And Run

The company has a capital program with advantaged prospects that send cash flow rocketing higher.

Introduction

Talos Energy, (TALO) has not gotten a lot of attention from this page. I looked at it a couple of times from the 30K foot level, but never drilled down on the company. The first time I looked it was in the $30's and I thought that was too high and moved on to other opportunities. The last time I looked it was in the single digits, seemingly range bound there for the past couple of years.

In recent time's it's followed the market higher with crude, and breached $20 to the upside for the first time in a couple of years. So the easy money has been missed in this company, darn the luck. The question before us is, does it have staying power at this level, and are there catalysts to move it higher?

Since this the first time to cover TALO we will do a fairly deep dive.

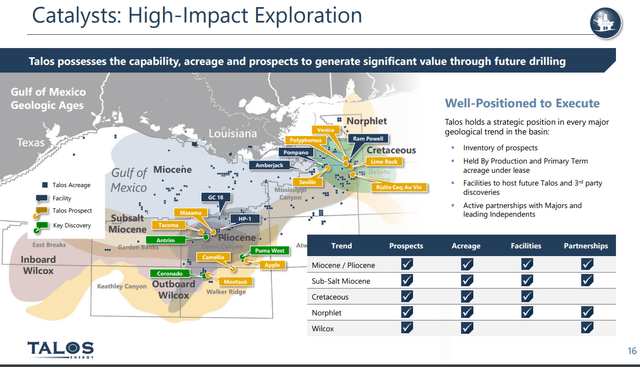

Why the Gulf Of Mexico-GoM?

I've been pounding the table with the notion that American energy assets are seriously underpriced for a long time now. It’s been the focus of a number of articles where I’ve developed this thesis, in the past. Mostly on another platform though, so you’ll just have to take my word that is well-trod territory for me.

The point is, that after 75-years of development, and 30 or so in deep water, the GoM is hugely blessed with the most abundent energy infrastructure anywhere in the world. It is also defended by the Coast Guard and the U.S. Navy. Nobody is going to be launching missiles at it, or hijacking a rig (I am resisting the urge to say many members of our own government would be glad to do that, but that is not productive, so I won't. I didn't say that! You didn’t read it. Capisce?)

The GoM is also blessed with abundent, layered low decline sandstone reservoirs in both shallow and deep water. The capital cost to develop many of the stranded field left behind by the big operators is relatively low and again, hugely advantages oil and gas exploration in this arena.

That's it in a nutshell.

The thesis for Talos

Talos bears some resemblance to another GoM operator we have covered recently, that being W&T Offshore, (WTI). (Which BTW has doubled since we presented to you.) As you can see they have a broad footprint in the GoM. Pompano, Amberjack, and Ram Powell are of late-90's deep water heritage, and sit in what is now puddle-depth waters, 1,200-1,500' deep. They were ground-breaking projects in their time, but soon exploration yielded successes in waters too deep for bottom supported tension-leg, platforms-TLP's. These platforms largley produce oil from satellite fields discovered near enough to run subsea tie-backs to the host. Technology has evolved to the point where these "pockets" of oil can be as far as twenty-five miles from the host, making a wide field of 1-20 mm bbl oil traps economic. That is Talos' stock in trade.

They are busy off Pompano with a platform rig targeting at least two wells this year. There is also an open water program using Seadrill's Sevan Louisiana Semi, with 6-well remit, three of which will lap over into 2023's capital budget. Successes from this program will also be piped back to Ram Powell, or Pompano. Tim Duncan, CEO comments on the potential impact of a discovery-

Each of these prospects are targeting 10 million to 30 million barrels equivalent gross and each are a one well subsea tieback that could deliver a gross initial production rate between 6,000 and 10,000 barrels equivalent per day per well. We expect them to be online between late 2023 and throughout 2024, depending on each projects timing.

Company filings

Stepping into deeper water we have several non-op wells, including an appraisal well of 2021's Puma West discovery in Green Canyon. BP is the operator of this well, with a nearby host at the Mad Dog SPAR, some 15 miles away. The Puma discovery well was suspended for a future completion if the appraisal well bears out, so far undisclosed, reserves estimates. Talos has a 25% working interest in this well, which is in an area where finds of several hunderd million barrels OOIP have been made.

Ok let's deal with Zama

Talos is learning the lessons of taking a bunch on money to a foreign country, particularly a Latin American country. Sometimes it just stays there. After making a billion-barrel find, Talos has had nothing but frustration, as cross-border unitization, and a change in the Mexican government's stance regarding foreign companies operating in their waters. The saga is pretty well documented in this SP Global article.

Talos won the block where Zama is located during the first auction organized by the prior Mexican administration of President Enrique Pena, which opened the sector for private investment for the first time after seven decades of Pemex monopoly. When it discovered Zama in 2017, Talos was the first private company to strike oil in over seven decades. After SENER's decision to grant operatorship of Zama to Pemex, Talos said it would consider all its options, legal or commercial to maximize value for its investors.

Talos has drilled multiple appraisal wells at Zama, while Pemex has not conducted any activity on its side of the reservoir, data from the National Hydrocarbons Commission shows. Early in June, the commission announced Pemex had cancelled the drilling of Asab 1, an exploratory well meant to provide more information on the nature of the shared reservoir in Pemex's side.

The decision to grant operatorship to Pemex was seen in Mexico as part of a series of moves by the administration of President Andres Manuel Lopez Obrador to give preference to the state company in an attempt to restore its dominance. The moves go against the existing regulatory framework that promotes liberalization and are being fought in courts.

Ouch. Needless to say Talos has pumped hundreds of millions into Zama. They retain a 17.5% interest if production ever sees the light of day. This quote by Tim Duncan, CEO of Talos pretty well sums up the situation-

"We have not 100% given up on Zama; we are doing absolutely everything given the circumstances to maximize value to shareholders, but we are going to keep looking for areas to replace it," CEO Timothy Duncan said during the company's second-quarter results call.

Recent diplomatic conversations between the Mexican government and our may hold out some hope for a resolution on Zama. One can only hope the team involved from our side wasn't the same intrepid crew that got spanked by the Chinese last year.

I have a fair amount of experience-not at this level to be sure, in Latin American countries.

Carbon Capture and Storage

We won't go into a great amount of detail on this topic. By now the aims of CCS and the intersectionality of the major IOCs in developing projects along the Gulf Coast have been discussed ad nauseum. The idea is that old, played out oilfields can be converted to Co2 injection is an alluring prospect that features prominently in conference calls. The fact that the refining, and petrochemical industry that is concentrated along the Louisiana and Texas coastal area provides an extensive customer base for these projects. P&A a few wells on older platforms to recover the slots, drill new wells designed as injectors, hook up a Co2 pipeline, and "Bob's your uncle," you are saving the planet.

I am going to let you in on a little secret. There is trouble in Paradise for this idea. It's funny how operators with the extensive resume in CCS that Chevron, (CVX)has, forget that after sucking hydrocarbons out of these reservoirs for a decade or more, changes have occurred. Witness CVX's travails in sunny (really sunny) North-Western Australia, as reported in an IEEFA article.

The construction of the CCS project, which is supposed to capture and store carbon dioxide that is extracted along with fossil gas from the Gorgon reserve, was a condition of Chevron’s approvals for the Gorgon LNG project. The project has consistently underperformed since it was commissioned in late 2019 – the commissioning itself was several years behind schedule.

One of the major issues impacting the project has been sand that has clogged parts of the CCS system, causing the project to significantly reduce the amount of carbon dioxide injected into the undersea reservoir.

Oh my heavens! Do they mean the sand that was mobilized by extracting oil and (mostly) gas, and finally water. Water contact is closely associated with the sand production that denotes the terminal phase of production from a well. So after 75-years of sand control learnings, Chevron is relearning this lesson? I don't want to be too strident here. Just be aware that numerous pitfalls (expensive ones at that) abound on the way to saving the planet.

I will close this section with the comment that injecting into a reservoir is a task of considerably more complexity than producing it. A lot of the blithe commentary around CCS injection cracks me up. Talos however, is quite giddy about all of this as Tim Duncan's commentary around bringing CVX into the Bayou Bend project denotes-

Lastly, this week we announced an expansion of our Bayou Bend project in Jefferson County, Texas with the preliminary agreement to bring Chevron into an expanded joint venture with the current partners Talos and Carbonvert. This transaction will include the consideration of cash and a capital carry that will cover Talos' costs through FID, which includes speed studies, a stratigraphic well test, activities related to classics permitting, and ultimately, final project approval.

Talos will remain the operator of the project and it is our belief that Chevron's reputation and commitment to investing in CCS-related projects will help kickstart this important hub. This is a major development that speaks to tangible success that Talos has achieved over the past year in its CCS initiative.

We look forward to collaborating Chevron in the coming months and years to make by Bayou Bend the premier CCS solution in the Beaumont Port Arthur industrial region of Southeast Texas.

Company filings

If anyone has Tim's email address, you might forward that IEEFA link to him.

Q-1, 2022 for Talos

The company generated $208 million of adjusted EBITDA during the quarter on ~63k BOE production, or $36.61 per barrel equivalent or adjusted EBITDA excluding hedge losses of $335 million or approximately $59 per barrel equivalent.

After approximately $85 million of capital expenditures in the quarter, Talos generated over $90 million of free cash flow before changes in working capital. Importantly, adjusted net income for the quarter was $64 million, or $0.77 per diluted share.

During the quarter, they paid down an additional $35 million on their credit facility and reduced leverage debt to 1.4 times net debt to EBITDA, down from 1.7 times at year end. The company's liquidity in cash and credit is ~$500 mm, with $450 mm available on their RBL.

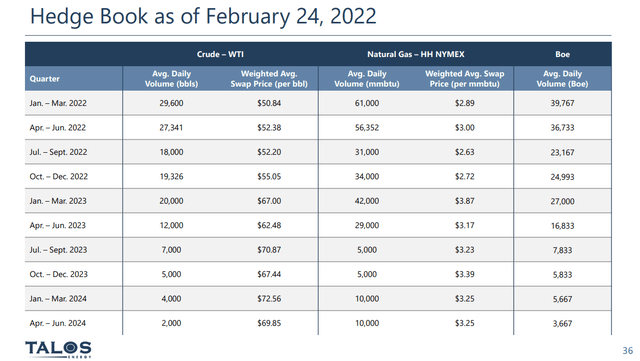

Hedges are costly in this environment where realized prices are in the mid $90's. As we have learned though, they help companies put a floor price enabling them to cover their costs reliably. They are also commonly stipulated by lenders. Talos seems to be getting a bit more risk-tolerant as the hedge book slide indicates.

Talos has no debt walls that will cause it to face liquidity problems in the current oil price environment. The subject of the 12% secured notes came up in the call. Management's commentary indicated that it's on the radar, but not keeping them up at night.

Your takeway

At current prices the company is trading at an unhedged EV/EBITDA multiple of just over 2X. That's pretty cheap. Tim Duncan, CEO agrees.

However, our valuation today reflects a steep discount to the value of our current production and does not give us credit for any of the value wedges of our business, namely our carbon capture business discovered resources such as Puma West and Zama and the value of our drilling portfolio. Today, I still see Talos as an incredible investment opportunity, one that I believe is amongst the best opportunities in the energy sector

Company filings

On a price to flowing barrels basis it trades at $39K per barrel. Puma West and any of several projects we have discussed could add 10-15K BOEPD on an individual basis. If their daily production notched up to just 70K BOEPD that would drop to $35K per barrel, with another $50 mm or so associated EBITDA. I will let you run with your imagination of what another 10-20K BOEPD might do to these ratios. All of this supports Duncan's theme that Talos shares are under-valued by the market.

Analyst's are bullish on Talos. Six of seven professional analysts covering the company have given it a BUY rating. Price targets range from $19, where it is currently to a median of $23, and an outlier of $40. Let's see how plausible that $40 is.

As hedges roll off in 2023, EBITDA could nearly double toward $2 bn on a run rate basis, assuming the price regime stays in its current range, and success in at least one of the projects now underway, not counting Puma West in this calculation. Puma could be huge, 20-30k BOEPD. To keep the multiple at 2X the shares would have to rerate to ~$36 per share, putting a reasonable target in range of that $40 estimate.

None of these estimates take into account Zama, or any of the CCS projects that will begin to come on line over the next couple of years. Talos will receive payments from the generators and the government for excuting these plans, and if things go well could be very lucrative.

In short in this very supportive environment I view Talos, even with the share price doubling that's occurred since December, to have a lot of room to run. Investors should carefully consider if a micro-cap like Talos deserves a place in their portfolios.

Disclosure. The author his long Talos.

Disclaimer. Nothing I say in this article should be construed as investment advice. It may look or sound like it, but it is not. I am not a CPA/CFA and have no formal training/certifications/licences in either discipline. In these articles I present analysis and relevant information that an interested investors may find instructive. I may be bullish, bearish, or neutral and will discuss why, but I am definitely not recommending you buy or sell any security I discuss. Investors should always do their own due diligence before plunking down their hard-earned cash. They alone are responsible for their investing decisions.