Kimball Royalty Partners: Put This One On Your List At A Lower Price

Kimball has good prospects but thing are higgledepiggeldy in the oil patch just now. If we see $12 again it might be time to jump on this one.

Kimbell Royalty Partners, (KRP) is down about 20% from highs established last fall, but has been in a fairly tight range since the first of the year. This is more a function of the oil and gas price sell off than any issue with the company. I see the company as a dividend play more than growth.

Royalty plays like Kimbell bring a natural advantage in that they just collect "rents"-royalties, without the cost implication of generating the capex needed to fund operations. There is a potential downside to essentially being a landlord, if the drillers fortunes decline, so too will those of the Royalty owner.

With that in mind let's take a closer look at Kimbell.

The thesis for Kimbell

As previously noted Kimbell has a well diversified footprint, with core areas in the Permian, Eagle Ford, and the Haynesville. With the slowdown occuring in the Haynesville, the company recently made an acquisition to augment its already substantial holdings in the Permian. The focus area for the MB Minerals deal is in Howard country where we know several operators are drilling intensely to grow production.

More broadly as you look at the slide above you see the company's payors consist of top tier, well-financed drillers in most cases.

Davis Ravanas, President and CFO comments on the MB Minerals pick up-

We expect to add approximately 1,900 BOE per day with a mix of 77% oil, 12% natural gas and 11% NGL based on our estimated run rate average daily production over the next 12 months.

These barrels were added at a fairly low multiple to strip pricing at 3.3X. The deal consisted of $43 mm in cash, and 5.93 mm new shares, with the total deal valued at $143 mm. These new barrels bring ~$52 mm in annual revenue and probably ~$40 mm in cash flow at $75 WTI. So it seems like a smart pick up, particularly if you remember no capex comes out of the cash flow, but goes straight to the bottom line. Much of that should show up in future dividend payments. Additionally, the MB Minerals pick up shifts weighting on their production mix from 29 to 34% in favor of oil.

The company has a history of being fairly nimble in sussing out new deals to grow output, so the drilling frenzy going on in Howard Country doesn't bother me excessively in terms of drillable inventory. This deal will pay out in less than 3-years, giving the company ready cash to look for new ones. I think the Permian consolidation is set to continues as the area matures and we are likely to see more of this "horse-trading." Mangagement matters as we have discussed, and Kimbell has done a good job of staying ahead of the decline curve.

Currently they are yielding just over 9%, after a 27% dividend cut from the prior quarter. This is associated with paying down debt during the quarter, a 15% dip distributable cash flow QoQ, and an increase in the common share count for the acquisition. The company seems to target a 9% YOC and adjusts its dividend to meet that target. KRP throws off a 1099, which makes them suitable for portfolios run out of retirement accounts.

If oil prices increase there is the potential for much healthier dividends as evidenced by the past year where prior quarters in 2022 saw $0.48, $0.49, $0.55, and $0.47 dividends respectively.

As I said, I see KRP as a high yield dividend play more than a significant growth opportunity. With their diverse portfolio and quality production, low PDP decline rates and upside drilling locations, the company has a long runway, and acts as a major consolidator in the gas oil and gas royalty sector.

Q-1 results

Revenues came to $57.4 mm, down ~10% from the prior quarter's $64.4 mm. DCF or Net Income landed out at $28.8 mm/79,800,000 or $0.35 per share. Their record first quarter run rate daily production of 17,014 BOE per day, an increase of 10.5% from Q4 2022, was composed of approximately 58% from natural gas and approximately 42% from liquids or 29% from oil and 13% from NGLs. Debt stands at $223 mm which is a fairly conservative ratio of 1X to 12 month TTM EBITDA. In addition to $28 mm in cash, KRP has $126 mm of availability on their revolver.

Kimbell's first quarter 2023 average realized price per barrel of oil was $74.99, per Mcf of natural gas is $3.16, per barrel of NGLs was $25.82 and per BOE combined was $36.19.

Expenses for Kimbell were $8.3 million in the quarter, $5.1 million of which was cash G&A expense or $3.34 per BOE. Unit based compensation in the first quarter, which is a non-cash G&A expense was $3.2 million or $2.07 per BOE

Guidance

They continue to expect oil production growth from US operators to remain relatively flat. In the call they noted, the number of DUCs in the US, which is one of the best indicators for near-term production growth, has dropped precipitously since 2020 and has not recovered. Nor are they expected to in the near term as operators will continue to focus on replenishing their DUC inventories in the short-term. That combined with inflationary pressures in the drilling completion and labor side of operators businesses will continue to temper oil production growth during 2023.

We also expect to continue benefiting from our diverse portfolio with quality production, low PDP decline rates-12%, and a high upside for new drilling locations. As a major consolidator in the highly fragmented US oil and gas royalty sector, we remain bullish about the long-term consolidation in this space and our role in it.

Risks

If oil and gas prices do not rise as expected, and drilling declines on their properties, cash flow could suffer. This would undoubtedly lead to declines in their share price and dividend payout.

Interest costs are on the rise, having nearly doubled from $3.3 mm to $5.1 mm QoQ. The company makes sporadic payments on their debt, as noted in the Q-1 report. This will have the effect of moderating further interest rate increases.

They now have 5.93 mm more common units to pay dividends on. That is going to make payout increases more challenging.

Your takeaway

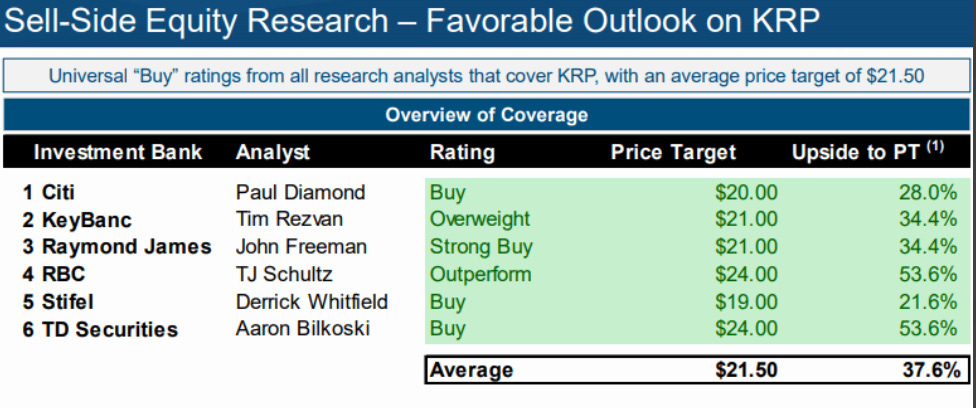

The seagulls have moderately aggressive price targets for the company as noted in the slide below. Price targets range from $19-$24 per share with a median of $21. Implied growth is 30-40%.

At 6.38X EV/EBITDA and $74K per flowing barrel, I find these aggressive price targets a little hard to justify. Particularly in light of a declining rig count in one of their key plays-the Haynesville, I think it could be a quarter or two before this one grows into it's current share price.

As such, I would rate it a hold if you have a current position and are willing to live with a fairly flat dividend for the next quarter or so. 9% is not a bad yield and is appropriate for the risks a small company like Kimbell carrys. If it hits the $12’s again, take a hard look.

Disclosure. The author has no position in KRP.

Disclaimer. Nothing I say in this article should be construed as investment advice. It may look or sound like it, but it is not. I am not a CPA/CFA and have no formal training/certifications/licences in either discipline. In these articles I present analysis and relevant information that an interested investors may find instructive. I may be bullish, bearish, or neutral and will discuss why, but I am definitely not recommending you buy or sell any security I discuss. Investors should always do their own due diligence before plunking down their hard-earned cash. They alone are responsible for their investing decisions.

Canada is similar, I can claim the with holding tax of 15%, this is not really a tax and I’m not certain Canada will let me deduct it. It’s a 10% fee on the sale, the IRS just started it Jan 2023.

I’ve had a couple of discussions with my broker, howler I won’t be buying any LP’s anytime soon. Will affect all non residents of USA, regardless the country they live in, at best I can claim it as a 10% broker fee, but not certain.

As a Canadian I have to stay away from any LP, the US initiated a fee in Jan 2023 and they take 10% of the sale value on any LP product, just sold some ET preferred, only had a small position, but its a preferred, paid 8 or 9% div annually. Of course a piece of the DIV is sliced off for tax, BUT I sold my position of 200 shares around $4900, I might even have had a small cap loss. Exactly 10% was taken, and as far as I can determine I can not get it back...and probably cant even deduct it off my Canadian taxes...