Crew Energy: Any Gas Left In The Tank?

Crew's production is primarily gas, and gas is selling fast these days.

Introduction

You don't have to look any farther to realize the strides the oil industry has made in the last year, than Crew Energy, (OTCQB:CWEGF). Crew is a Canadian micro-cap gas producer with operations in the Montney play we have discussed many times. Over the course of the last year it had quintupled in price, falling back in May as the gas price pulled back from the $9's. We'll take a quadruple any day. It was in the low $4’s when this article first came out, but has rallied sharply higher to near $5.00 in the last week or so.

Much of this growth has been the result of the surge in gas price, but Crew has been doing their part to firm up value. In 2021 reserves grew 20% YoY, and the company has continued that pace in 2022 with Q-1 reserves rising 27% over the same period last year. Currently the company is focused on high impact returns, deleveraging, and cost reduction as opposed to shareholder returns.

Crew's production is heavily weighted to gas, condensate, and NGL's, with production of the latter two rising 45% and 19% respectively. The 2022 capital program remaining centers on the high impact Groundbirch acreage, where they will drill 5-producing wells. We will take a closer look at Groundbirch in the catalyst section of this article.

Crew represents an attractive entry point its current price, and investors looking for growth should consider if the company meets their risk profile.

The thesis for Crew

Crew's Montney acreage footprint meets our requirement of being blocky and connected as the slide below illustrates. It also is more upper Montney as opposed to lower Montney, meaning cheaper drilling costs. As this is frac country connected acreage, the most important factor in reducing well costs, makes longer laterals possible and lowers cost per foot. It should be noted that the bulk of Crew's acreage is silty-sandstone that features lower declines than shale. Sandstones have connected pore structures that promote horizontal flow and higher natural permeability. As we have discussed in the past, this features leads to lower declines, shorter payouts, and improved ROCE.

They have a lot of room for expansion of their production footprint, with 3,000 Montney drill sites located. Crew's acreage is also advantaged as regards takeaway with access to several pipelines serving Canada's West Coast, and the Southern and Eastern U.S.

Against a strong backdrop for gas globally, Crew is well posistioned to ride the crest of a long wave. Energy needs in Europe and the developing world provide an increasing element of demand for gas producers like Crew. Front month contracts for gas are above $8.00 USD through Feb of 2023, reinforcing the backwardation that has been in place for the last couple of years.

A potential catalyst for 2022

Crew noted in their earnings press release that they had drilled and completed five wells. The first three that have been turned in line are exceeding the Proved plus Probable area type curve forecasts reflected in Crew’s year-end 2021 independent reserves evaluation, with an average per well raw gas production rate after 180 days (“IP180”) of 8,593 mcf per day. At 360 days this well shows production of about 2.5 mm mcf/d, which is still pretty good and could continue for another year before eventually watering-out.

Management commented on the potential impact of these Groundbirch wells in the press release-

Crew owns over 70,000 net acres of contiguous land in the Greater Groundbirch area. The Upper Montney at Groundbirch is approximately 470 feet in thickness and has four prospective zones, two of which have been tested on the initial three well pad. Two additional zones are expected to be evaluated in the last half of 2022 with the completion of our five well pad.

Q-1, 2022 for Crew

Crew produced boe per day (200 mmcfe) average production in Q1/22, a 27% increase over Q1/21 and a 15% sequential increase from Q4/21, marking a new Company record.

Q1/22 natural gas production increased 33% to 159 mmcf per day, condensate production increased 45% to 3,926 bbls per day and natural gas liquids (“NGLs”) increased 19% to 2,856 bbls per day, compared to Q1/21

Q1/22 natural gas production increased 33% to 159 mmcf per day, condensate production increased 45% to 3,926 bbls per day and natural gas liquids (“NGLs”) increased 19% to 2,856 bbls per day, compared to Q1/21.

This production enabled $77.7 million of Adjusted Funds Flow (“AFF”) ($0.51 per share basic share and $0.48 per fully diluted share) was generated in Q1/22, a 128% increase over Q1/21 and a 66% sequential increase from Q4/21, driven by significant production growth and strong operating netbacks of $28.83 per boe. The Company’s goal to improve margins was proven successful with an AFF to petroleum and natural gas sales ratio of 60% in Q1/22 compared to a 40% ratio in Q1/21.

Free AFF of $22.3 million was generated in Q1/22, affording Crew flexibility in capital allocation with the ability to direct Free AFF to repay debt and fund future growth to enhance financial sustainability.

22% reduction in cash costs per boe to $9.61 per boe in Q1/22 from $12.25 in Q1/21, reflecting the successful advancement of one of the goals within our Two-Year Plan, to reduce cash costs per boe to between $9.00 and $10.00 per boe from 2020 to 2022. Net operating costs per boe were reduced by 25% in Q1/22 to total $3.50 per boe, compared to $4.65 per boe in Q1/21.

$55.4 million of net capital expenditures in Q1/22, directed to an active exploration and development program that resulted in Crew drilling five (5.0 net) and completing six (6.0 net) natural gas wells. The Q1/22 capital program continued to leverage cost and operational improvements, with reduced drill times and strong capital efficiencies.

55% improvement in Crew’s net debt to last twelve-month (“LTM”) to EBITDA ratio, which was 2.0 times at the end of Q1/22 compared to 4.4 times at the end of Q4/21. Net debt at quarter-end was reduced to $392.4 million, a $13.6 million improvement compared to year-end 2021.

Increased bank facility, after completing the Company’s annual renewal, extending the facility’s maturity through to June 2024 and increased the borrowing base by 23% to $185 million.

Source

Your takeaway

Crew is holding production flat for 2022, in the range of 31-33K BOEPD. Analysts are moderately bullish on Crew, giving it an over-weight rating, and a price target of CAD$6-8.75 over the next year. That's a potential uplift of 50% in USD. With production held steady growth will come from margin improvement in cost control. They have established a pretty good track record here as noted below.

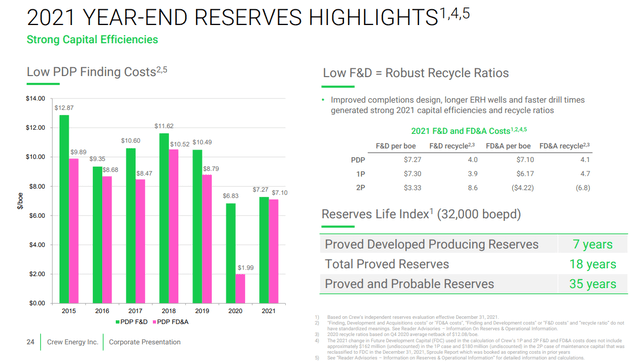

They don't disclose a lot about their operations or completions philosophy, but the notes in the slide above stipulate "improved completions design, longer Extended Reach Horizontal-ERH, and faster drill times are associated strongly with improving these metrics.

On an EV/AFF basis the company is trading at a multiple of ~3X. Flowing barrel ratio is on the low side at $28K per barrel of production. Both of these numbers are at a discount to peers in this play. The company also trades at a discount to 1P Reserves at $3.6 bn compared to an EV of ~CAD$960 mm.

Using those metrics, there is no way this company isn't a BUY.

Investors with moderate risk tolerance and a 1-2 year time horizon should carefully consider if Crew fits in their portfolio.

Disclosure. The author has no position in Crew Energy.

Disclaimer. Nothing I say in this article should be construed as investment advice. It may look or sound like it, but it is not. I am not a CPA/CFA and have no formal training/certifications/licences in either discipline. In these articles I present analysis and relevant information that an interested investors may find instructive. I may be bullish, bearish, or neutral and will discuss why, but I am definitely not recommending you buy or sell any security I discuss. Investors should always do their own due diligence before plunking down their hard-earned cash. They alone are responsible for their investing decisions.